GST OVERVIEW

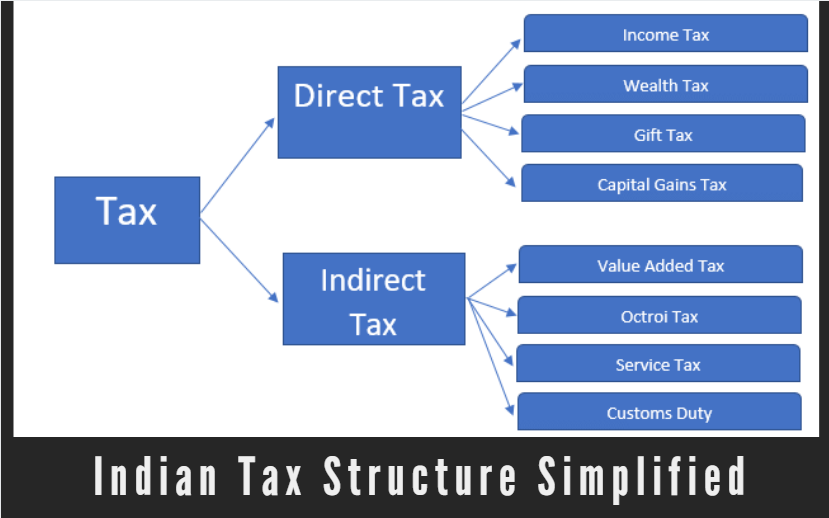

The present indirect tax regime is complex and entails multiple taxes and duties. Further, there is a significant cascading effect of taxes on account of various restrictions on cross utilization of credit of one tax against another. In addition to this, the multiplicity of returns and compliances at State level, administrative costs, waybills requirement for inter-state movement of goods, add to the procedural compliances to be followed by the assesses.

Introduction of a GST to replace the existing multiple tax structures of Centre and State taxes are not only desirable but imperative in the emerging economic environment. The Goods and Services Tax (GST) is a destination-based value-added tax, levied at all points in the supply chain with credit allowed for tax paid on purchases used in making the supply. It would apply to both goods and services in a comprehensive manner with exemptions restricted to a minimum.

The dual GST which would be implemented in India will subsume many consumption-based taxes. At the central level, Central excise duty, Additional excise duty, Service tax, Countervailing duty (CVD) and Special Additional Duty (SAD) and at State level, VAT/Sales tax, Octroi and Entry Tax, Purchase tax, Luxury tax, Entertainment tax and taxes on lottery, betting and gambling would be subsumed.

Rate Structure under GST

| Rate | Description |

|---|---|

| 3% | Precious items like Gold and Silver |

| 5% | Essential items |

| 12% | Standard rate |

| 18% | For goods other than covered under 12% |

| 28% | Luxury goods |

A 4-tire GST tax structure of 5, 12, 18 and 28 percent, with lower rates for essential items and the highest for luxury and demerits goods that would also attract an additional cess, was decided by the GST Council. By removing the cascading effects, layers of taxes, and simplifying the structure, GST will effectively mean that the tax paid by the final consumer will come down in most cases. In case of services it is likely expected to have a flat rate of 18% including cesses.

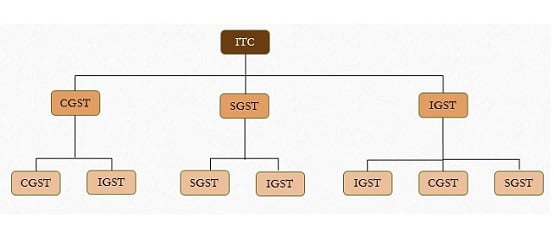

Tax Credit Mechanism

Cross-utilization of credit of CGST between goods and services would be allowed. Similarly, the facility of cross utilization of credit will be available in case of SGST. However, the cross utilization of CGST and SGST would not be allowed except in the case of inter-State supply of goods and services under the IGST model.